PUBLIC FINANCE (hacienda.gob.mx)

On September 8, 2023, the Federal Executive, through the Ministry of Finance and Public Credit (SHCP), delivered to the Congress of the Union for the corresponding legislative process the Economic Package for 2024, which is the last budget of the current administration.

The Package is presented without proposing or proposing modifications to the fiscal legal framework; therefore, no taxes are created nor are current rates increased, i.e., there are no changes to the Income Tax (ISR), Value Added Tax (VAT), Special Tax on Production and Services (IEPS) laws, nor to the Federal Fiscal Code (CFF), The bill includes only the General Economic Policy Criteria (CGPE) and the Initiatives to the Federal Income Law (LIF), the Federal Law on Duties (LFD) and the Federal Expenditure Budget (PEF).

As a preamble to the presentation of the Package, the Executive has pointed out in accordance with the CGPE that the results obtained during the same and what has allowed that it has not been necessary to increase or create new taxes derive from a responsible tax policy, since the current Administration in its beginnings implemented some of the collection measures to increase tax revenues that were being analyzed and worked on in previous Administrations, making changes in the tax regulatory framework towards a progressive tax system to combat social inequality, also indicating that among the actions carried out, or well implemented, are the elimination of universal compensation, the classification of tax fraud as a serious crime, the adaptation of the tax framework to the digital economy, the implementation of measures of the BEPS (Base Erotion, Profit Shifting) project of the OECD (reportable schemes, neutralization of hybrid schemes and the limitation of base erosion through interest), the establishment of anti-abuse rules, and the elimination of write-offs.

In this regard, the Executive Branch points out that the characteristics of the 2024 Economic Package include the consolidation of a welfare state, forecasting a 2.5% to 3.5% real annual economic growth based on consumption and employment, as well as the continuity of the fiscal policy that will allow the public debt balance to be sustainable, guaranteeing the strength of tax collection to avoid tax evasion and avoidance through the LIF and favoring social welfare through austerity, efficiency and rationality in public finance spending through the PEF.

In general terms, it should be noted that it is expected that, in the LIF, on the one hand, there will be no changes in the tax incentives established and, on the other hand, that an increase in the withholding rate on interest paid by the financial system will be established.

According to the deadlines of the legislative process, the draft of the LIF initiative must be approved by October 31 at the latest, while the PEF must be approved by the Chamber of Deputies by November 15 at the latest.

In addition, although there are no modifications to the current legal fiscal framework, it is important to take into account the following for 2024:

1) Outsourcing of specialized services.

a) Renewal of the Registry of Providers of Specialized Services or Specialized Works (REPSE).

As a result of the 2021 labor reform regarding the subcontracting of specialized services, the Ministry of Labor and Social Welfare (STPS) created the public registry known as REPSE, which, on the one hand, is mandatory for all employers that provide specialized services other than the corporate purpose of their clients, among other characteristics, On the other hand, it is valid for 3 years, so that any individual or legal entity that is registered in the registry must keep in mind that during the fiscal year 2024 and, in particular, during the second half of the year, it must process the first renewal of its registration, if it was made for the first time in 2021 and it was not cancelled. REPSE STPS.

It is important to mention that the validity of the registration is mandatory and necessary to operate legally when rendering and/or receiving specialized services, in addition to the fact that, among others, the REPSE is an indispensable requirement in tax matters and, specifically, for the deduction of payments made and the crediting of VAT for this type of services.

2) International Taxation

Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting . (Known as "MLI": Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting or Multilateral Instrument MLI). beps-mli-position-mexico.pdf (oecd.org)

As of January 1, 2024, the MLI will be effective in Mexico, provided that each country with which Mexico has a treaty has also concluded its domestic processes, initiates its effectiveness and considers Mexico as a treaty covered by the MLI.

The provisions of the MLI will apply to each tax treaty entered into by Mexico (except for the United States of America and Germany) to form part of it, functioning as a protocol, even if they are not integrated in the same document, to jointly interpret and execute such treaty and the MLI as a single agreement. In other words, the MLI will include regulations for the precision of treaty concepts for their better application, as well as for the interpretation of particular clauses and their technical aspects, with the objective of avoiding the erosion of the tax base, the diversion of benefits by multinational companies, and the abuse of treaties or treaty shopping through structures whose sole objective is to benefit from the treaties without there being a justification of the need for the operation, that have no business reason and, One of the most important changes of the MLI is that it includes the concept of the principal purpose test (commonly abbreviated as PPT), so that most of the tax treaties entered into by Mexico will contain provisions that will deny the obtaining of treaty benefits if it is considered that the obtaining of a tax benefit was the main or one of the main purposes of the corresponding transaction.

In this sense, although there may be differences with each country covered, the entry into force of the MLI will have effects on transactions with foreign residents and on the planning for individuals who have investments abroad, so it is important to review and comply with its provisions in order to have access to the benefits of the treaties and in turn not have contingencies to deduct the respective payments.

It is worth mentioning that, among others, the MLI includes regulations on double residence, beneficial ownership, related third parties, specific rules for dividends and capital gains, fragmented or split contracts for permanent establishment purposes, control of hybrid schemes, as well as the review of income that is not taxed at source (business profits), to verify when treaty benefits will or will not be applicable.

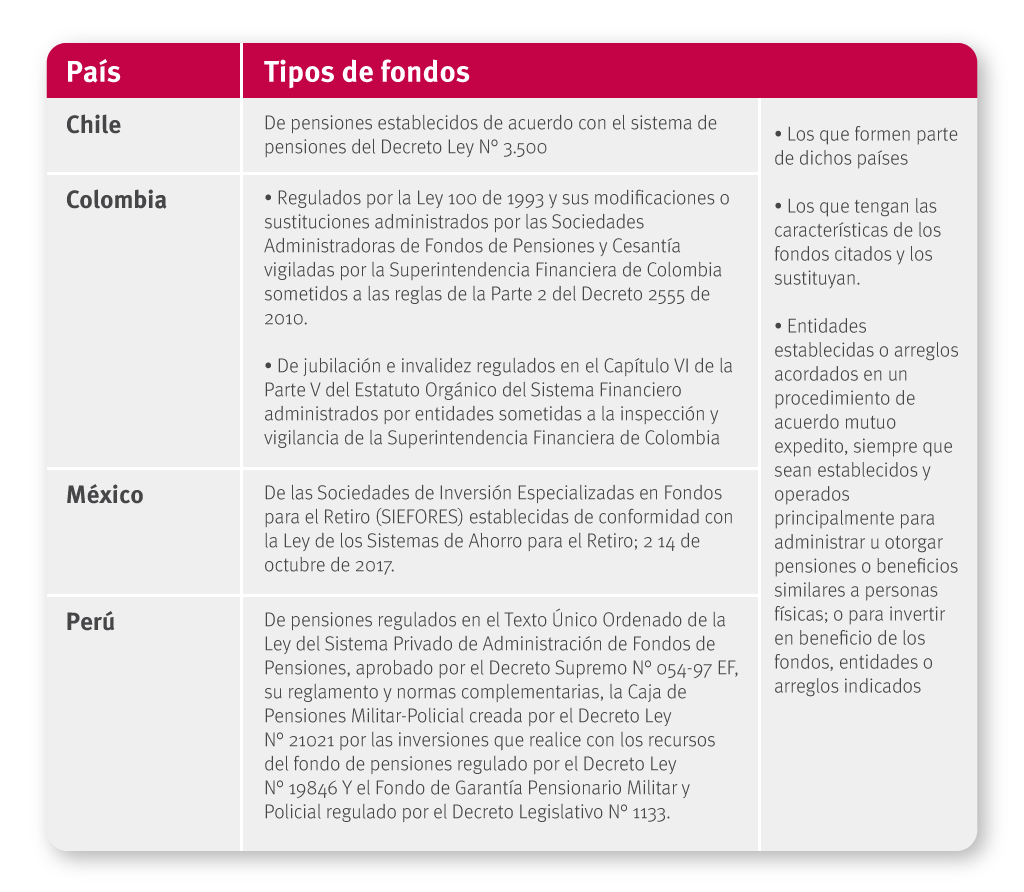

a) Pacific Alliance

As from January 1, 2024, the Convention to avoid double taxation of the Pacific Alliance, formed by Colombia, Chile, Mexico and Peru, will also be applicable, which modifies the bilateral agreements to avoid double taxation subscribed between said countries, on the one hand, granting resident status to pension funds for the purposes of applying said agreements and obtaining the tax benefits foreseen in said bilateral agreements and, on the other hand, equalizing the tax treatment for income from pension funds for the purposes of applying said agreements and obtaining the tax benefits foreseen in said bilateral agreements, The agreement amends the bilateral agreements to avoid double taxation signed between these countries, on the one hand, granting the status of residents to pension funds for the purposes of the application of these agreements and obtaining the tax benefits provided in these bilateral agreements, and on the other hand, equating the tax treatment for interest income and capital gains from the sale of shares made through a stock exchange that is part of the Latin American Integrated Market (MILA) and received by the pension funds. CONVENTION TO AVOID DOUBLE TAXATION OF THE PACIFIC ALLIANCE ENTERED INTO FORCE AND WILL BEGIN TO APPLY FROM NEXT JANUARY 1 (http://www.gob.mx).